What to Expect From a Roof Insurance Claim in Connecticut

A realistic look at the CT roof insurance claim process from filing to final payment, including timelines, coverage types, deductibles, and what homeowners should prepare for.

Most West Hartford homeowners have never filed a roof insurance claim, and the process can feel overwhelming the first time around. Between adjuster inspections, depreciation holdbacks, and supplement requests, there are several stages that catch people off guard when they are not prepared.

Understanding what actually happens at each phase removes the guesswork and helps you avoid costly mistakes. This guide walks through the realistic timeline, the financial details that matter most, and the documentation standards that lead to fair outcomes.

How Connecticut Policies Handle Roof Damage

Before you file anything, it helps to know what your policy actually covers. Connecticut homeowner policies respond to sudden and accidental damage from specific named perils. The key covered events include wind, hail, fire, falling tree limbs, and the weight of ice or snow.

What policies will not cover is equally important. Normal wear and tear, age-related deterioration, deferred maintenance, and manufacturer defects all fall outside the scope of a standard claim. The Connecticut Department of Insurance has noted that insurers are increasingly scrutinizing roofs older than 15 years before policy renewals, making it even more important to understand your coverage before a storm hits.

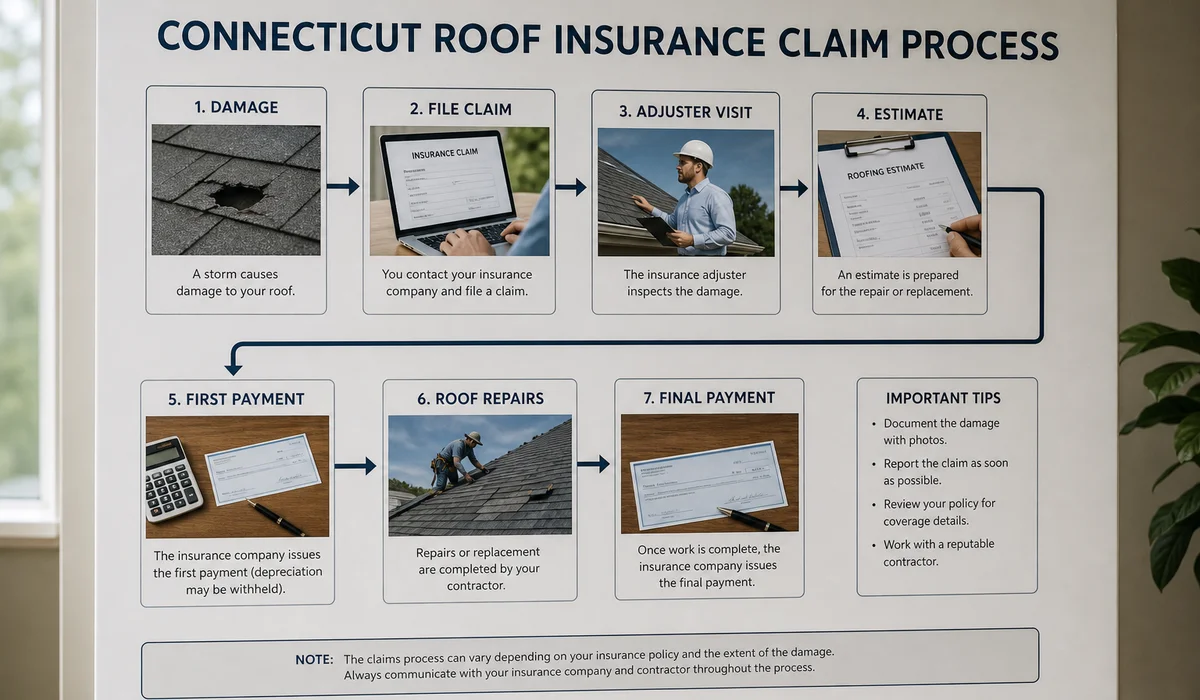

Realistic Timeline From Filing to Final Payment

The entire roof insurance claim Connecticut homeowners go through typically takes four to eight weeks from the initial call to the final depreciation recovery check. Here is what each stage looks like in practice.

Days 1-2: Emergency Response and Documentation

Your first responsibility after storm damage is preventing further loss. Your policy requires you to mitigate ongoing damage, so emergency tarping or temporary repairs should happen immediately. The carrier typically reimburses these costs as long as you keep receipts.

At the same time, photograph every damaged area before any cleanup. Capture wide shots of the full roof plane, close-ups of missing or cracked shingles, interior water stains, and any debris on the property. This initial documentation becomes the foundation of your entire claim.

Days 3-10: Claim Filing and Adjuster Inspection

Once you call your carrier, they assign a claim number and schedule an adjuster visit. Expect the inspection within two to seven business days, though heavy storm seasons can push that timeline to two weeks or longer when adjusters are handling high volumes across Hartford County.

The adjuster produces a scope and estimate using Xactimate, the industry-standard pricing software. For 2026, typical Connecticut roof repair costs range from $400 for minor patching to $1,300 for significant repairs. Full replacements with architectural shingles generally fall between $11,200 and $20,700.

Weeks 2-4: Payment and Repair Scheduling

After the carrier approves the estimate, they issue the first payment. Under RCV policies, this initial check represents the actual cash value after depreciation. Under ACV policies, this is your only payment.

West Hartford Roofing coordinates the repair schedule once funding is confirmed, typically beginning work within one to two weeks of approval depending on material availability and weather conditions.

Weeks 4-8: Completion and Depreciation Recovery

After repairs are finished and final invoices are submitted, RCV policyholders receive the withheld depreciation amount. This second payment closes the gap between the depreciated value and the actual replacement cost. Expect this final check within two to four weeks of submitting completion documentation.

ACV vs. RCV: The Financial Reality

The single most important number in your claim is whether you carry Actual Cash Value or Replacement Cost Value coverage. The difference can mean thousands of dollars out of pocket.

| Coverage Type | How It Pays | Example on a $15,000 Roof |

|---|---|---|

| ACV (Actual Cash Value) | Pays only the depreciated value based on the roof’s age and condition. | A 20-year-old roof might yield $6,000. You cover the remaining $9,000 yourself. |

| RCV (Replacement Cost Value) | Pays the full replacement cost in two installments, minus your deductible. | You receive $6,000 initially, then the $9,000 recoverable depreciation after repairs are complete. |

Check your policy declaration page now, before storm season arrives. Knowing which type you carry determines how much financial exposure you actually face.

Deductibles and Wind/Hail Triggers in West Hartford

Many homeowners assume their standard deductible applies to all claims, but wind and hail events often carry a separate, percentage-based deductible. These are typically 1% to 5% of your total dwelling coverage rather than a flat dollar amount.

For a home insured at $500,000 with a 1% wind/hail deductible, that means $5,000 out of pocket before the carrier pays anything. This catches many residents off guard during severe storm seasons.

Under Connecticut law, a hurricane deductible only triggers when the National Weather Service officially measures sustained surface winds of 74 miles per hour or more within the state.

If the storm does not meet that official threshold, your standard lower deductible applies instead.

Code Upgrades and Supplement Requests

Older homes across West Hartford, particularly the Colonials and Tudors built in the 1920s through 1960s, frequently require code upgrades during a roof replacement. The 2022 Connecticut State Building Code mandates an ice barrier extending at least 24 inches inside the exterior wall line under Section R905.17.4. Additional requirements may include improved attic ventilation and upgraded decking.

Without a “law and ordinance” endorsement on your policy, these mandated upgrades become your responsibility. That can add $3,000 or more to the final bill.

Supplements address hidden damage that the initial adjuster inspection missed. The most common supplemental items include rotted plywood decking discovered during tear-off, concealed flashing damage, and interior water damage revealed after opening ceilings. Filing supplements with thorough photo documentation and line-item pricing is critical to receiving full compensation.

When the Carrier Pushes Back

Disputes are not uncommon. Carriers may argue that damage results from wear rather than a storm event, that the roof’s age exceeds their internal threshold, or that the total damage does not justify full replacement. Multiple prior claims on the same property also draw extra scrutiny.

Strong documentation is your best defense in any contested claim. Timestamped photos, detailed contractor reports, and weather data from the specific storm event all strengthen your position. For tactical guidance on navigating adjuster interactions, our guide on working with an insurance adjuster covers the process in detail.

Preparing for a Smooth Claim

The homeowners who navigate this process most successfully are the ones who prepare before a storm arrives. Review your policy declaration page annually, confirm whether you carry ACV or RCV coverage, understand your wind/hail deductible, and verify that you have law and ordinance coverage.

Our storm damage roof repair service includes full documentation support and direct adjuster coordination throughout every phase of the ct roof claim process. If you have active leaks or fresh storm damage, contact us for an emergency inspection while the evidence is still clear. Starting the process early with proper documentation gives you the strongest foundation for a fair outcome.

Frequently Asked Questions

What is the difference between ACV and replacement cost coverage? ▼

ACV (Actual Cash Value) pays only the depreciated value of your roof based on its age. Replacement Cost Value (RCV) pays the full cost to replace it, typically in two installments. RCV is significantly better for homeowners facing a major claim.

Will filing a single claim increase my premium? ▼

One storm-damage claim usually has a minimal effect on premiums. However, filing multiple claims within a few years can lead to noticeable rate increases or even non-renewal.

Does insurance cover leaks from an aging roof? ▼

No. Standard homeowner policies only cover sudden and accidental damage from named perils like wind or hail. Gradual deterioration, deferred maintenance, and age-related wear are excluded.

Ready to talk to a roofer?

Read about our storm damage roof repair service or get a free estimate.

Related Guides

What to Do Immediately After Roof Storm Damage

A concrete action plan for the first 72 hours after roof storm damage - safety protocols, interior containment, documentation, emergency repair, and insurance filing with realistic durations.

How to Document Roof Storm Damage for a Claim

A concrete step-by-step process for documenting roof storm damage that gets insurance claims approved - photo checklists, dating evidence, receipts, and professional reports.

Emergency Roof Tarping: When It's Needed

Know when emergency roof tarping is the right call and when a direct repair makes more sense. Decision framework for West Hartford and Hartford County homeowners.

What to Expect When Working With a Roof Insurance Adjuster

A realistic guide to the adjuster inspection process for CT roof claims, covering contractor coordination, test square methodology, disputed scopes, and supplement filing.